Suppose you want an option (the right, but not the obligation) to exchange a risky asset 2 for a risky asset 1 at the time of maturity. Margrabe’s formula, a generalization of Black-Scholes for two-assets, is an option pricing formula to value said option: enhanced with security computation, it allows to exchange private assets.

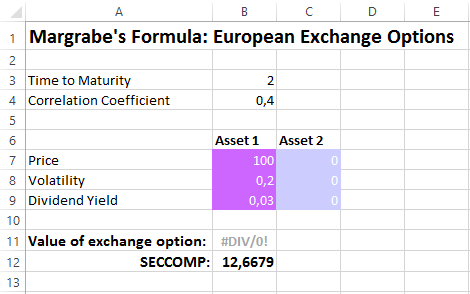

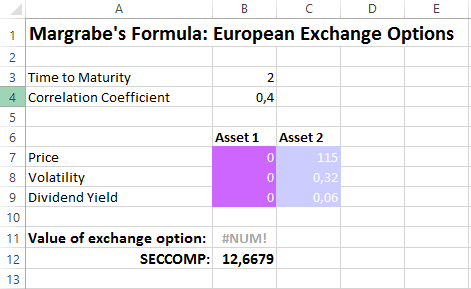

On one side, the first party specifies the current price of the asset, its annualized volatility and the dividend yield:

On the other side, the second party specifies its corresponding price, volatility and dividend yield:

Together, they securely compute the value of the exchange option of two private assets.

DISCLAIMER

The preceding is just a simplified example for illustrative purposes. In the real world, you will have to change the concrete parameters and use more complex formulas.